Transitioning from renting to owning a home in Canada is no small feat but, even so, according to the Royal LePage Canadian Renters Survey (June 2025), over 50% of renters plan to transition to owners, with over one third looking to do so in the next two years.

Thinking about making the jump yourself? As local Realtors, we help first-time buyers in Ottawa understand their options and navigate the process with confidence. Feel free to reach out if you’re curious about what’s possible for you.

Myth 1: You’ll NEVER own a home.

I’m sure you’ve been bombarded with people telling you you’ll never transition from renting into ownership. You’ve likely heard that there’s no way to save at a fast enough rate while also paying rent, that housing prices in Ontario are far too high and that home ownership is unattainable. The “what ifs” in your mind are likely plentiful and, frankly, pretty convincing.

But here’s the thing, if you listen to that noise, you’ll never make the leap. Of course, not all scenarios are so cut and dry but for the most part, the transition IS possible. Don’t doubt yourself so much that you aren’t willing to try. Flip those “what ifs” around and ask yourself, “what if I never explore my options?” or “what if I’m missing out on my opportunity to buy my first home?”.

Again, we understand this is easier said than done and every situation is unique but there’s no harm in exploring your options.

Myth 2: Lenders treat your rent as a debt when applying for a mortgage.

Lenders do not look at your current rent in the same way they look at loans or credit card debt. Lenders WILL use your rental history as a baseline for your affordability and as a track record for consistent housing payment. Your rental history will have also helped you build a strong credit score which will all work toward helping you get approved for a mortgage.

Lenders WILL look at:

- Your total household income (if you’re purchasing with a partner, family member or friend).

- Your Credit Score

- Your Current Debts (including car loans, student loans, credit card debts, etc.)

- Your Total Down Payment (remember your savings will need to go toward lawyers fees & closing costs as well).

If you’re not sure where to start or want a clearer picture of your buying power in Ottawa, we’d be happy to sit down with you, review your situation, and give you a roadmap to your first home.

Some key things to look at to prepare for the possibility of homeownership include:

- Your Credit Score (a higher credit score will help you when it comes time for mortgage approval).

- Your Savings (this is what you’ll use for a downpayment. Consider looking at what you currently have, what you’re willing to use and how you can budget to add to your savings).

- Your Income (Calculate your household income if you plan to buy with a partner, friend or family member).

- Your Expenses (including loans, lifestyle/habits, credit cards, etc.).

You want to have a full financial picture drawn out to get an accurate idea of where you’re starting on this journey. When it comes time for mortgage pre-approval you’ll want to have a baseline for your monthly budget. The biggest mistake we see clients make is maxing out their budget based on their highest mortgage approval amount. You need to take your lifestyle and spending habits into account to set a realistic budget.

Part of our job as your Realtors is to help you line up the right team of mortgage specialists and financial advisors, so your approval stays intact and you’re protected every step of the way.

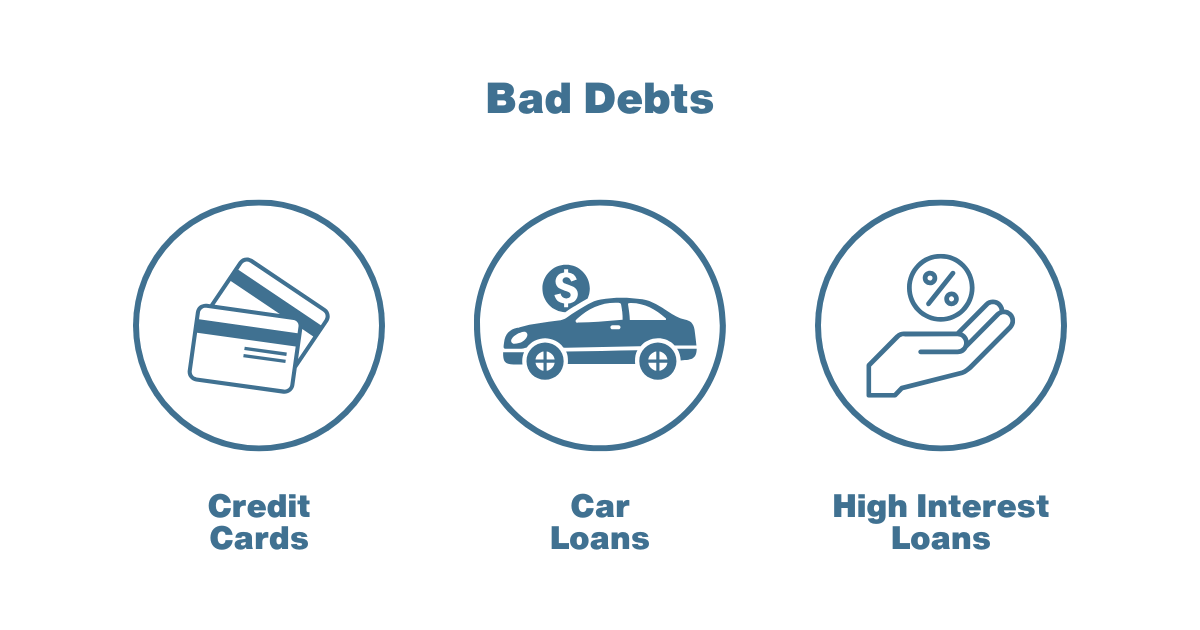

Myth 3: All Debts Are Bad Debts!

Let’s say, like 34% of Canadian renters (Royal LePage Canadian Renters Survey, June 2025), you plan to buy a home in the next two years. The best way to prepare for homeownership is to understand what lenders will be looking for when it comes time for Pre-Approval.

As mentioned above, lenders will not treat your monthly rent as a debt, however they will look at things like credit card debt, student loans, car loans, etc. If you want to buy a home it’s best to get these debts under control so that they aren’t used to calculate your Total Debt to Service Ratio (which is your total debts compared income) when being approved for a mortgage.

Mortgage professionals like to say there are “good debts” and “bad debts”. The term “good debts” seems like an oxy-moron but in the case of mortgage approval some debts can be helpful. As we mentioned before, your rent can help you build a strong credit score and so can debts, like student loans.

Student loans are considered a “good debt” because it’s financing an income earning investment, this means your education should (in theory) lead you to a higher income & stable employment. When considering student debts during mortgage approval, lenders will look at your monthly payment amount not the full amount owed.

For example, if your minimum monthly payment is $300 when applying for a mortgage, your lender will only consider that amount rather than, let’s say, the $15,000 left on the loan. If you’re making consistent monthly payments, you’ll build a strong credit score– another positive when it comes to mortgage approval.

What IS considered a bad debt?

Anything that’s financing a depreciating asset, like a car loan for example. Cars are a depreciating asset, meaning their value begins to decrease from the moment you purchase them. What does this mean? Avoid getting a car with a high monthly payment. It’s tempting when car dealerships advertise no interest monthly payments but that monthly payment will be considered a debt when applying for a mortgage.

Credit card debt may be the worst debt of all when it comes to mortgage approval. Credit card debt can severely limit your borrowing capacity, heavily impact your credit score and usually comes with extremely high interest rates compared to other debts/loans.

Again, credit card debt is a non-productive debt and can be a red flag for lenders because you’re spending money that you seemingly don’t have. If you have credit card debt, paying it off should be your first priority when it comes to preparing for homeownership.

If you’re not sure what the best way to rectify your debts before a mortgage application is, talk to a financial advisor or mortgage professional. They can give you tailored advice regarding a path to homeownership. If you’re looking for reputable & trusted advisors in Ottawa, reach out to us! We can put you in contact with a team of professionals.

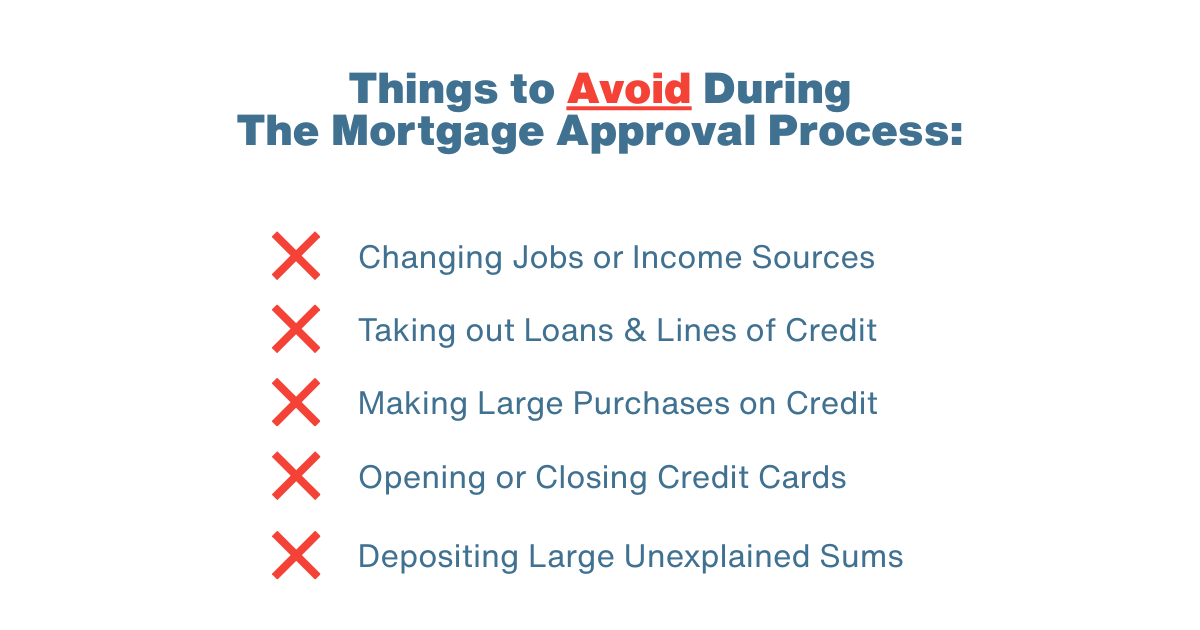

Myth 4: Once I’m Pre-Approved, I’m Guaranteed A Mortgage.

Think of your pre-approval as a snapshot in time. A pre-approval is based on the information given (income, debts, employment, etc.), at the time to your lender. If any of those circumstances were to change, for example, you change jobs or you finance a car, at the time of applying for your actual mortgage, you may not be approved.

Your actual mortgage application will be based on the specific property you wish to purchase, your financial situation at the time of application and current interest rates. With all of these variables, your approval amount may change.

Now, the good news is that your pre-approved interest rate will typically be locked in for 90-days from the time you were approved. So, even if interest rates rise while you’re shopping for your home, you’ll be able to claim your approved rate when purchasing.

The most common misconception about your pre-approval is that it’s guaranteed but the caveat here is that your financial position needs to remain unchanged. Avoid expensive credit card bills, switching jobs, taking out loans or financing vehicles/big-ticket items until you’ve closed on your property.

Myth 5: Renting is ALWAYS cheaper than owning.

On paper, this may be true. We get it, you see you can rent a two bedroom home for $2200 per month, while the monthly mortgage amount on the same home would be $2975. It seems like renting saves you $775 per month, but is it actually?

Your monthly expenses may be lower, but you’re not building equity which is the benefit of homeownership. The thought with homeownership is that your monthly expenses (while in some cases more expensive than renting) will be repaid when you sell the property down the line.

While you may not always make a profit from the sale of your home, you are likely to offset a large portion of what you would have spent on rent over the same period.

Wondering what this could look like for your own situation? We can run the numbers based on your budget and location so you see exactly what’s realistic.

Now, there are some caveats to this. Appreciation is not guaranteed. Home values can fluctuate — some years may see strong growth, while others may experience a decline. The longer you hold your property, the better your potential return, which is why we typically recommend a 5–10 year horizon.

Interest rates also play a major role. While many homeowners choose a 5-year fixed rate, those on variable-rate mortgages should be prepared for changes at renewal.

The truth is, renting can offer flexibility and fewer responsibilities compared to homeownership. It’s not “wasted” money, it’s paying for a roof over your head and can make sense during life transitions or uncertain job situations. It’s important to understand the ups and downs of homeownership compared to renting when deciding which path makes sense for you.

Ready To Take the Leap?

Stepping into homeownership is a lifestyle and financial shift. While renting offers flexibility, owning gives you the opportunity to put your money toward your own future instead of someone else’s.

Yes, the process can feel overwhelming at first but with the right plan and guidance, it becomes much more manageable. The key is taking it one step at a time, surrounding yourself with professionals who have your back, and making decisions based on what’s right for you.

If you’re ready to explore your options or simply want to chat through your situation, our team is ready to help. Reach out anytime.