“Will the Canadian housing market crash in 2024?”

“Will the housing market crash in 2025?”

“We’re headed for a market crash!”

You’ve probably read a few dozen headlines like this over the last few months and if you’re a homeowner, prospective buyer or investor, you might get a pang of anxiety in your gut with every mention of a housing market crash.

Here’s the thing, there’s been speculation about the Canadian housing market crashing for the last few years. In fact, in September of 2022, we wrote a blog post similar to this one outlining a history of Canada’s housing market crashes because even then, the world was convinced that a crash was looming.

As we said back in 2022, there’s no way to predict a housing market crash with absolute certainty. However, there are some tell-tale signs that something is coming.

Here’s Your Guide to How & Why Housing Market Crashes Happen

First, for a true housing market crash, very specific economic conditions must be present. It’s a combination of factors that lead to full market failure. Having some “symptoms” of a crash isn’t necessarily an indicator that the floor is going to fall out from underneath us. In Canada, we have a very strict lending system that helps protect borrowers from being overleveraged and reduces the possibility of a full housing market crash.

If you take a look at the history of Canadian housing market crashes, you’ll see that almost every time it failed, we put new systems and protocols in place to prevent these scenarios from happening again. So, with the current protections we have in place, a full market crash is unlikely, but not impossible.

Here’s our list of the 3 significant indicators of a housing market crash.

Home Prices are Rapidly Rising & Affordability is Decreasing

This is probably the most obvious indicator but when housing prices rise well above the income levels of a country, it’s definitely going to impact borrowers’ ability to purchase property. When this happens, it’s referred to as a “housing bubble”.

In Canada, we’ve definitely felt this across almost all housing markets. When prices hit their peak in 2022, we saw a lot of people over-leveraged and panic selling when they couldn’t afford their mortgages, especially people who bought at the peak of COVID and were up for renewal or were on variable-rate mortgages as the interest rates started rapidly rising to curb inflation.

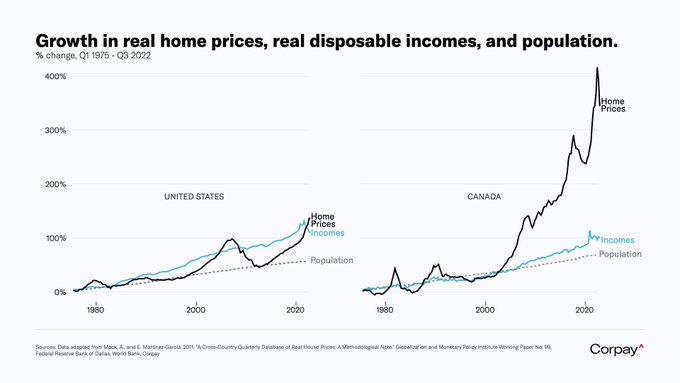

Since interest rates were rising, home sales slowed, and prices began to dip. We watched throughout 2023 as housing prices in major markets decreased significantly. Even so, housing prices still far outpace income levels in terms of growth (see chart below).

If you’re panicking right now reading this and thinking it shows the Canadian housing market is doomed, don’t be so sure. A lot of markets are seeing a slow return of buyers which is helping to put upward pressure on prices once again. In fact, Royal LePage is predicting that we will see an increased average sale price by the end of this year (2024).

Declining Demand and High Inventory Levels

This one is a bit of a no-brainer; if no one’s buying, you’re going to have a hard time selling.

While we saw demand dwindle throughout 2023 and the beginning of 2024, we’re seeing demand increase as prices stabilize and interest rates slowly lower.

Right now in Ottawa, we have about 4.5 months of inventory on the market, which is below the long-term average of 5 months. So, overall we aren’t seeing inventory fall into the “too high” range.

Keep in mind, across Canada we have a housing supply shortage, which is actually one of the leading causes of inflated housing prices.

Increasing Interest Rates

When interest rates are on the rise, we see a few things happen:

First, would be first-time buyers standing on the sidelines waiting for rates to lower. We saw this throughout 2023 when the Bank of Canada increased the key lending rate to 5% and held it for months on end.

Second, we see homeowners with a renewal period coming up unable to afford their mortgage with their new interest rate. We’ve seen this happen over the last year or so when a lot of those COVID-19 mortgages with 1-2% interest rates came up for renewal when rates were upwards of 5%.

Both of these situations lead to decreased demand and offloading of properties which leads to lower housing prices and can indicate a crash is near if rates continue to rise.

Thankfully, the Bank of Canada began slowly lowering rates this year, and we’ve seen buyers warm up to the idea of entering the market. The key interest rate in Canada now sits at 4.25% (as of September 4, 2024), a drop of 75 basis points since June 2024 after holding it at 5% since July 2023.

So, Will The Canadian Housing Market Crash?

As we said, we can’t predict what will happen to the housing market with absolute certainty. However, we do know that prices are still rising at modest rates, inventory is at or below the long-term average and with interest rates steadily lowering, buyers are returning to the table.

In our humble opinion, the Canadian market, and more specifically, the Ottawa housing market, will not crash anytime soon. We’re seeing steady activity and more confident buyers every day. If trends continue as they are, we should be safe from a full market crash.

We hope learning a bit more about what contributes to a housing market crash has helped ease your anxiety. Whether you’re a homeowner, first-time buyer or investor, we hope you’re walking away from reading this with a little more confidence.

If you live in Ottawa and are looking to enter the market, contact us! We’re ready to help you reach your real estate goals and answer any questions you might have about the market or your specific situation.

Don’t forget to follow us on social media to stay in the loop with market updates, tips and more!