Homeownership can provide an owner plenty of opportunities besides a roof over their head. It provides borrowing power. Once you build up your home’s equity, it can be a source of funds in the event you need money.

There are two main ways people can pull equity from their home without having to sell, that’s through a Home Equity Line of Credit (HELOC) or a Home Equity Loan.

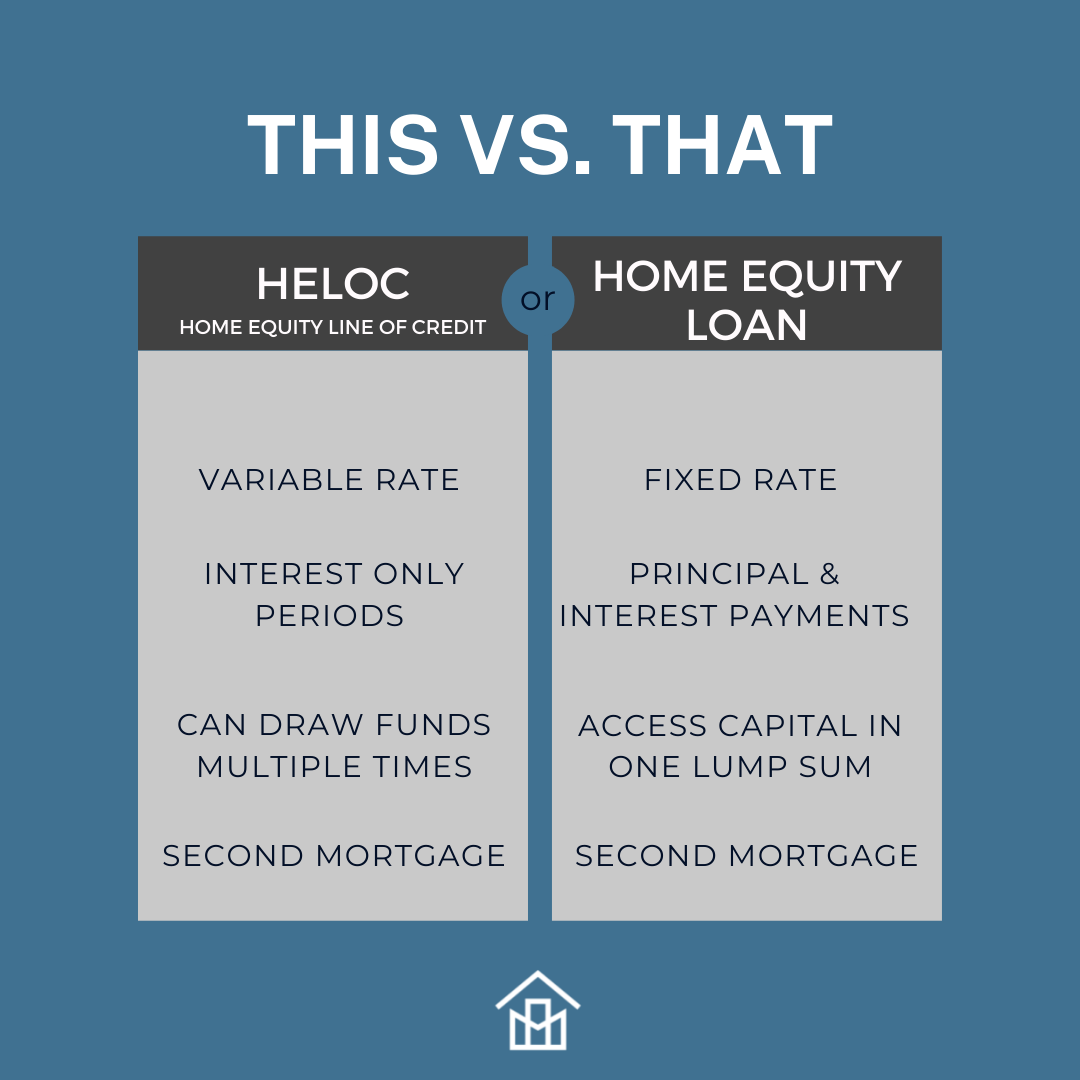

What’s a Home Equity Loan?

A second mortgage that allows you to access real estate equity in one lump sum. After the loan closing, the lender either cuts a check for a lump sum or wires funds to the borrower.

For example, if your home is worth $300,000 with a $200,000 mortgage balance, you would potentially be able to tap into $100,000 in equity.

Note: some home equity loans allow you to borrow up to the full 100 percent of your available equity, but others cap it at 85 percent or 90 percent. Also, keep in mind that these loans come with fixed interest rates.

These loans can essentially be used for anything, though typically, people use the funds to pay off more considerable expenses, including car payments & property down payments.

What’s a Home Equity Line of Credit (HELOC)?

This differs from a home equity loan in that you can borrow what you need but potentially take more later. Like a credit card, you only pay interest on the money you are using.

In the same example as before, where you have $100,000 in equity, you could get a line of credit for that $100,000. The difference is if you only use $60,000 of that credit, you only pay interest on the $60,000.

These lines of credit can come with variable interest rates & typically have grace periods of interest-only payments.

Biggest differences?

With home equity loans, the amount of credit available to you is as high as your available equity is. Alternatively, under a HELOC, the amount you get depends on your credit score, among other factors. This makes a HELOC harder to qualify for.

Another critical difference between the two options is the fixed vs. variable interest rates, which can drastically affect the payment amounts. Remember, you pay interest on the entire loan when it comes to a Home Equity Loan.

Both options can be a great way of utilizing your home’s equity; it’s just a matter of personal preference and/or circumstances. Talk to a financial advisor about your options when it comes to utilizing your home’s equity.